A few weeks back I considered the deflationary risk weighing on the global economy. A discussion on the This Is Money podcast, and comments from the BoE have taken me in the other direction this week. Why would we end up with high inflation and high interest rates?

First we need to talk about debt. Consumer debt has actually seen a record fall since the start of Coronavirus, something to do with not being able to spend and no need to keep up with the Jones’ (1). The same can’t be said for Government debt. As I write this The Economist’s Global Debt Clock is rising through $61,594,467,000,000 (2). This was a problem before COVID-19. 2019 saw record global debt to GDP ratios (322%), following slight falls in 2017 and 2018 (3, 4). China’s ballooning debt was of particular concern, with plenty of tenuous business loans supporting growth (4, 5).

The word addiction had been bandied about with reference to debt. Below is a favourite short that I use to explain addiction when doing teaching sessions about the dangers of gambling and drugs. You come to rely on the object of abuse to feel normal. Credit cards and lifestyle anyone?

Credit: Andreas Hykade, Filmbilder & Friends (6)

The reasons for increasing debt woes are country specific. In Europe and the US it’s a combination of household spending, QE and zombie companies. There’s the massive junk bond bubble scare brewing; corporations kept going in 2008/9 through borrowed money now being refinanced, on the verge of reaching junk bond status, at the same time low yields push people to riskier bonds in aid of returns (7, 8, 9). Yet people keep buying bonds (10). China is just straight up building infrastructure projects that are getting abandoned or never used, while Japan can’t get it’s GDP to grow (11). Individual investors continue to seek returns. Interest rates on savings are minimal, with decent returns disappearing (12, 13). Bizarre investment structures, like this Buy-to-Let-Cars scheme, hoover up those desperate for income on their holdings (14).

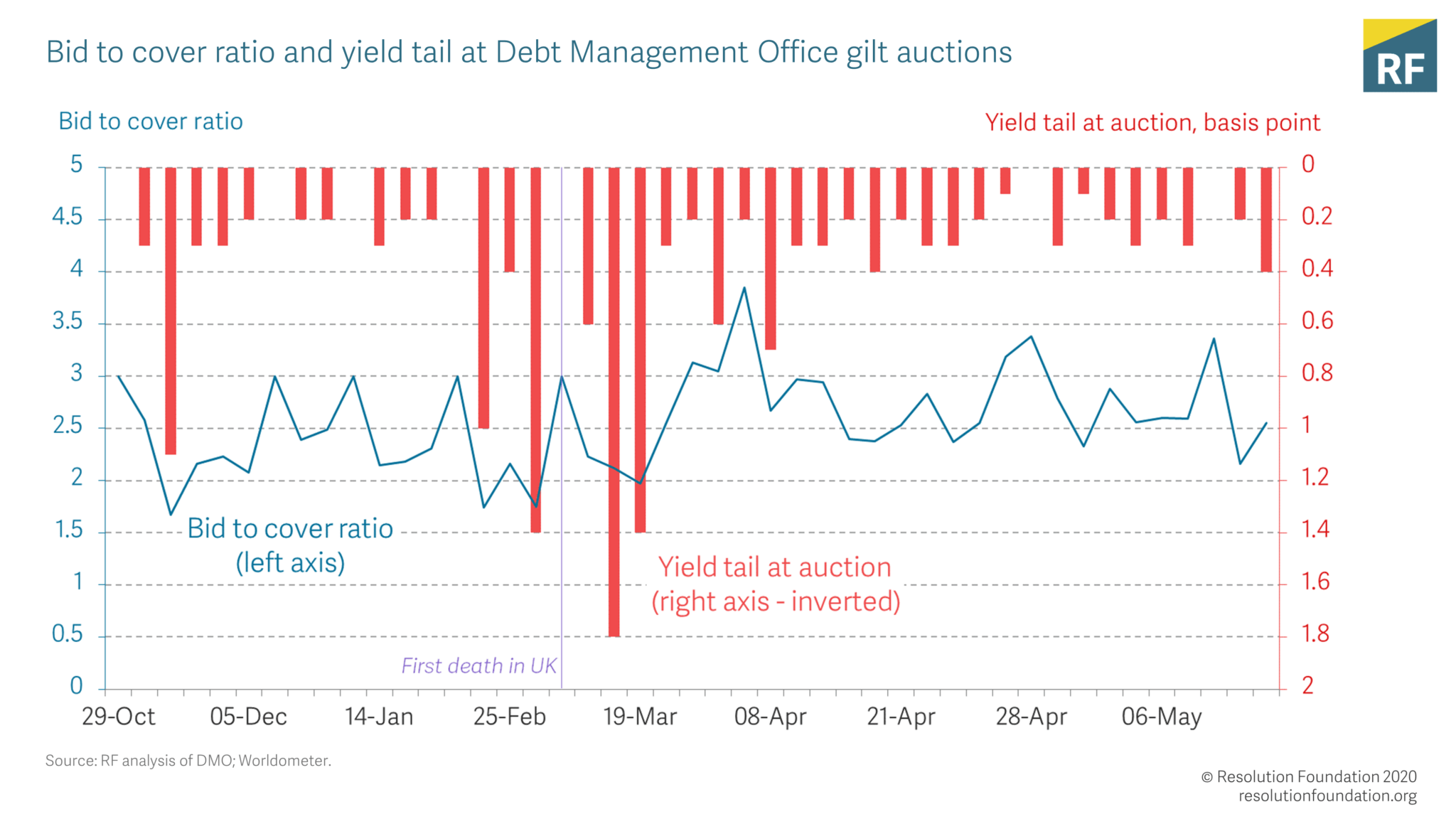

And then there’s COVID-19. The Government were very happy to deny a massive money tree for the NHS/ social care. Then they’ve opened their metaphorical chequebook and are handing round a whole forest of blank cheques. Which is needed. But the cost could be £298 billion in debt for Apr 2020/21 alone (15). Analysis from the Resolution Foundation suggests that currently £80 billion has been raised with no deterioration in cover ratio (16). Predictions therein suggest a further extension to QE in June (16).

Image Credit: Resolution Foundation (16)

So we’ve got a mounting pile of government debt as we borrow our way out of trouble. Low, or even negative interest rates are helpful for the Gov here. Favourable to continue borrowing. As TA at Monevator covered this week, we’re seeing some negative UK bond yields (17). The noise from the BoE is that proper negative interest rates are unlikely, but not impossible (18). Certainly there’s no push towards an interest rate rise (19).

Why should there be. Inflation sits at 0.8% for April 2020,(20) well below the BoE’s goal 2.0%. We’re worryingly close to stagflation; rising prices due to rising demand with static growth (21). There’s an argument that there’s a lot of pent up demand due to lockdown, with limited supply also thanks to lockdown. The QE money creation rears it’s head. Deflation is a feedback loop international governments definitely do not want (22). It will only increase their debts.

The magic bullet

So what about inflation. Measures of inflation like the CPI may not have spiked since the 2008/9 financial crisis because Joe Bloggs in his northern terrace has practically seen little inflation of prices. Consumer goods have probably decreased in cost. But the high ticket items like sports car, larger houses in certain postcodes, watches, wine, art and even gold have all risen in price.* The QE wealth got stuck on it’s trickle-down in high net worth owner’s assets. It created a high net worth inflationary micro-environment.

How are we getting out of this mess? A survey of top UK economists suggests that they feel there is no need to tackle public debt soon, and tax increases may the best method in the end (23). We can keep borrowing in the short term. In the long term there is the suggestion that inflation is the only sensible answer (24). QE and other factors are likely to push towards inflation anyway (25). Running inflation higher than 2.0% would reduce that Government debt burden. This method has been used before; after the second world war inflation ran at 4-5% for a good couple of decades (26).

My generation is just not used to that sort of inflation. One of my takeaways from The Intelligent Investor is the change in financial policy/climate. Graham wrote in a period where 4-5% inflation was not unheard of, and savings accounts could yield 5-7%. I vaguely remember those sort of numbers from my childhood building society, but I’ve never been conscious of that financial world. The risk of a 1970s/ Weimar Republic style inflation spike is present (27). The fear of that sort of inflation seems greater than the 1950s 4-5%, maybe due to recency bias, or because those with the most to lose are those who remember the 1970s (28).

Ultimately it seems we’re unlikely to see interest rates or inflation change in the short term. But maybe, in the medium-long term, we’ll see 5% interest rates again. We’re preparing for such eventualities (29). We can tolerate up to 12% on our mortgage with some belt-tightening. I’m sure many can’t. Those zombie companies would go to the wall. The BTLs may struggle. Perhaps a period of 4-5% inflation is the economic reset we need.

Have a great week,

The Shrink

*Gold is slightly more interesting because of just how much the price has rocketed, the argument for it’s use as a hedge, and it generally being the ultimate lesser fool’s gambit (30, 31). No-one wants to be left holding the hottest potato.

N.B. Again, as a more involved speculative post, I would love feedback and opinions on these thoughts.

News:

- A decent meta-analysis and systematic review in the Lancet of physical measures to reduce COVID-19 spread (32)

- House prices are unsurprisingly falling in response to lockdown (33)

Comment:

- Jase at FIRE Lifestyle has his May financial update (34) – With a massive savings rate to boot

- As does Firevlondon (35)

- And the Saving Ninja in report #23 (36)

- Early Retirement in the UK (37)

- Playing with FIRE (38)

- The Obvious Investors P2P investment monthly updates are always interesting (39)

- While Michael at Foxy Monkey has a review of his Property Partner investing so far (40)

- While back on the May updates, here’s Weenie’s (41)

- And Money Mage’s (42)

- The Ways, at A Way to Less (43)

- The Squirreler’s (44)

- And Sam from A Simple Life with Sam (45)

- The DIY Investor UK adds McPhy Energy to his portfolio (46)

- The IT Investor looks at 20 Global Investment Trusts (47)

- Life After the Daily Grind looks at buying second hand to avoid depreciation on household items (48)

- TI at Monevator on the flood of new investors (49)

- The Banker on FIRE tries to shed some light on the market nonsense, and behind closed doors trading (50)

- And why you won’t become a grizzled executive, and that’s no bad thing (51)

- MedFI explores inflation and it’s effect on it’s finances (52) – A nice combo with this post

- Monevator’s weekend reading has a brief comment on the current market upswing (53)

- Igniting FIRE is focusing more on the things they enjoy (54)

- Dr FIRE reflects on the financial successes of their 20s (55)

- Money Side Up has some thoughts on he effect of Coronavirus on the FIRE movement as a whole (56)

- Hustle Escape examines hindsight bias (57)

- And, finally, John at UKVI runs through the importance and methods of assessing dividend coverage (58)

References:

- https://www.thisismoney.co.uk/money/cardsloans/article-8380019/Consumer-debt-falls-record-7-4bn-April-borrowing-spend-slumps.html

- https://www.economist.com/content/global_debt_clock

- https://edition.cnn.com/2020/01/13/economy/global-debt-record/index.html

- https://blogs.imf.org/2019/12/17/new-data-on-world-debt-a-dive-into-country-numbers/

- https://www.ft.com/content/d93a95d0-2ee9-11e9-80d2-7b637a9e1ba1

- https://www.youtube.com/watch?v=HUngLgGRJpo

- https://en.wikipedia.org/wiki/Corporate_debt_bubble

- https://www.independent.co.uk/voices/coronavirus-economy-wall-street-debt-boeing-shares-junk-a9513176.html#gsc.tab=0

- https://www.barrons.com/articles/the-corporate-debt-death-spiral-shows-no-signs-of-stopping-51584023200

- https://www.cnbc.com/2020/02/07/junk-bond-scare-is-rising-no-one-cares-people-are-buying-everything.html

- https://www.forbes.com/sites/peterpham/2017/11/24/why-are-we-addicted-to-debt/#136e4b2515fd

- https://www.thisismoney.co.uk/money/saving/article-8381231/Top-fixed-rates-disappearing-Average-account-pays-just-0-3.html

- https://www.theguardian.com/money/2020/jun/05/savers-uk-covid-19-lockdown-cash

- https://www.buy2letcars.com/

- https://www.bbc.co.uk/news/business-52663523

- https://www.resolutionfoundation.org/publications/the-economic-effects-of-coronavirus-in-the-uk/

- https://monevator.com/negative-yields-bonds/

- https://www.thisismoney.co.uk/money/news/article-8357383/BoE-not-remotely-close-decision-negative-rates-Haldane.html

- https://moneytothemasses.com/owning-a-home/interest-rate-forecasts/latest-interest-rate-predictions-when-will-rates-rise

- https://tradingeconomics.com/united-kingdom/inflation-cpi

- https://www.theguardian.com/business/2020/may/31/for-all-his-woes-at-least-sunak-does-not-need-to-worry-about-stagflation

- https://foreignpolicy.com/2020/04/29/federal-reserve-global-economy-coronavirus-pandemic-inflation-terminal-deflation-is-coming/

- https://cfmsurvey.org/surveys/covid-19-and-uk-public-finances

- https://www.independent.co.uk/news/business/news/coronavirus-recession-bank-england-inflation-mandate-change-jim-o-neill-a9539796.html#gsc.tab=0

- https://moneyweek.com/economy/global-economy/601179/heres-why-the-coronavirus-crash-is-likely-to-end-in-inflation

- https://www.bloomberg.com/opinion/articles/2020-05-07/inflation-is-the-way-to-pay-off-coronavirus-debt

- https://simplelivingsomerset.wordpress.com/2011/03/15/when-money-dies-a-1975-cautionary-tale-from-the-weimar-republic/

- https://simplelivingsomerset.wordpress.com/2020/06/03/at-some-point-during-this-bear-market-i-realized-that-i-probably-shouldnt-keep-doing-this/

- https://www.moneyadviceservice.org.uk/en/articles/how-to-prepare-for-an-interest-rate-rise

- https://fee.org/articles/which-is-the-best-inflation-indicator-gold-oil-or-the-commodity-spot-index/

- https://pureadmin.qub.ac.uk/ws/portalfiles/portal/120196463/gold_inflation_s.pdf

- https://www.thelancet.com/journals/lancet/article/PIIS0140-6736(20)31142-9/fulltext

- https://www.thisismoney.co.uk/money/news/article-8372271/Homes-face-14-price-slump-says-Nationwide.html

- https://firelifestyle.co.uk/2020/06/01/may-2020-financial-update/

- https://firevlondon.com/2020/06/02/may-2020-a-sunny-month/

- https://thesavingninja.com/savings-report-23-back-to-break-even/

- http://earlyretirementinuk.blogspot.com/2020/06/end-of-month-report-1st-of-june.html

- https://playingwithfire.uk/may-2020-savings-and-spending-update/

- https://obviousinvestor.com/p2p-lending-portfolio-update-for-may-2020/

- https://www.foxymonkey.com/property-partner-coronavirus/

- http://quietlysaving.co.uk/2020/05/31/may-2020-plus-other-updates/

- https://www.moneymage.net/2020-may-savings-report/

- https://awaytoless.com/monthly-spending-may-2020/

- https://thesquirreler.com/2020/06/06/may-2020-net-worth-update/

- https://asimplelifewithsam.com/2020/06/06/may-review/

- http://diyinvestoruk.blogspot.com/2020/06/mcphy-energy-portfolio-addition.html

- https://www.itinvestor.co.uk/2020/06/20-global-investment-trusts-compared/

- https://lifeafterthedailygrind.com/buying-used-electronics-can-earn-you-money/

- https://monevator.com/what-is-behind-the-coronavirus-trading-boom/

- http://bankeronfire.com/who-is-smarter-than-the-stock-market

- http://bankeronfire.com/it-wont-happen-to-you

- https://medfiblog.wordpress.com/2020/06/05/chasing-inflation/

- https://monevator.com/weekend-reading-boom/

- https://igniting-fire.com/2020/06/05/the-joy-of-creation/

- https://drfire.co.uk/building-wealth-in-my-20s-successes-and-failures/

- https://money-side-up.com/will-coronavirus-infect-the-fire-retire-early-movement/

- https://hustleescape.com/hindsight-bias/

- https://www.ukvalueinvestor.com/2020/06/dividends-and-dividend-cover.html/

Speculativeness is good, I am all for it!

> savings accounts could yield 5-7%

Yeah, I remember them. Hell, I used to ram my credit cards up to the max using credit card cheques into a savings account, because you could get interest free periods and at savings rates of a few percent it was work the tiresome admin to stay on top of it all.

> But maybe, in the medium-long term, we’ll see 5% interest rates again. We’re preparing for such eventualities. We can tolerate up to 12% on our mortgage with some belt-tightening. I’m sure many can’t.

Pah. 12%. Curmudgeonly old git mode on – You whippersnappers don’t know you were born 😉 COGM off. I bought a house towards the end of the 1980s, I discharged my mortgage about 20 years later.l For the majority of my mortgage paying career I was paying at what is the long-term average interest rate for the UK, which is 6% or thereabouts. I was chuffed to get a capped montage at 6.5% in 1999 ISTR. Couple of years after I foolishly bought that first house, I was paying a shade under 15% interest, as I saw both sides repossessed and lose their homes.

Terrible times, people might say. But there was a corollary. If you kept your job, and you stayed in the asset class, the high interest rates kept house prices down because people couldn’t afford to bid prices up to stupid o’clock, and inflation eroded the value of the capital over the normal 25-year term. I borrowed 80% on that first house, and sold it for less than the mortgage to move, but over time interest rates came down and people drove house prices sky high, which saved my tail from the most monumental personal finance mistake of my entire life – buying a house at the wrong time.

Higher interest rates may have an interesting effect on house prices. Sure, inflation will help that look not so bad in the long run, but people with high LTVs before the heft in interest rates need to be able to service their mortgages long enough to get to the long run. Else hello crystallised negative equity, and potential bankruptcy. It happened in the early 1990s.

LikeLike

Hello Ermine, I hoped you would post. I was fully reflecting on your mortgage interest experience. I remember my parents scratching around to make payments in the early 90s. I can see us getting back to the long-run 6% average, much closer to Ben Graham’s written material. Having rerun our numbers, we could service up to 20% by increasing our term. Who else could?

We’re at a point where there’s a lot of cans been kicked down the road, all of which get seriously butthurt by increased interest rates; BTLs, 95% mortgages, the general low income/ inconsistent work pattern of the current Uber/Deliveroo/IR35 workplace, not to mention the zombie companies.

We’ve not had a hard reset in a long time. Deflation or spiralling inflation would be one. I wonder if a gradual taper up of interest rates may be a softer reset whilst resolving some of the general economic instabilities.

Vague hope.

LikeLike

I believe Schumpeter called it creative destruction. BTL – should be shot at dawn, old men should not compete with their children for an existential resource simply because they have more financial capital. Earlier generations had lending controls for just that reason, as well as keeping banks out of the market. Lenders gonna lend, and that means high house prices. At a party someone was bemoaning that their kids couldn’t afford to buy a house in the same breath as saying how well they had done from BTL so I asked “ever joined the dots?” 😉 Zombie companies – they have stolen 10 years of some of our creative minds which could have been applied to something we actually wanted.

We can’t step in the same river twice, the postwar period was probably one of a kind, but interest rates of 5% or so are useful. They to point capital at projects that make a decent return and get it to work. They penalize zombie uses, by bankrupting the miscreants.

> the general low income/ inconsistent work pattern of the current Uber/Deliveroo/IR35

Now that’s a tougher one. Some things have changed, the power has shifted greatly to capital from labour. Some of that problem could be fixed, and may be fixable. I’d personally surtax middlemen, particularly extractive platforms (Uber, Deliveroo, Amazon, I’m looking at you), employment agencies. Once upon a time companies employed everyone directly – from the janitors to the CEO. Nowadays there are fleas upon fleas – middlemen who subcontract to other middlemen, who outsource staffing to an agency, each parasitic layer skimming off their cut to provide a small number of BS jobs and make everybody else poorer. Some would argue modern companies are more flexible and fleeter of foot, but if it is bought by immiserating a large part of the population then either we need to do something about the companies or we need more creative alternatives like a universal basic income, to free people to tell these companies to get on their bike.

But there are deeper problems afoot. The economy simply doesn’t need people of low ability, and physical grunt is less needed than in the past. When I was a kid there were loads of people on a typical building site. When I say the Olympic Village being constructed 8 years ago it was a couple of hundred, tops. There’d be that many people building an estate of 10 houses in my childhood. The skils bar for getting work is rising- and globalisation was pushing the lower-end jobs overseas anyway.

I would say governments will do their best to try and make this a ramp. Perhaps they will manage. If not, there will be hell to pay.

LikeLiked by 2 people